中国男人,一年喝了80亿的东鹏特饮

本篇文章源自微信公众号:DT商业观察,ID:DTcaijing;文 字:张晨阳、数 据:张晨阳、编 辑:唐也钦 设 计:戚桐珲、运 营:苏洪锐 监 制:唐也钦。

2003年10月,潮汕人林木勤所在的国营饮料厂濒临破产,恰逢国企改制潮,他一咬牙出资267万元,把老厂子改制成为一家民营企业,主要售卖能量饮料。

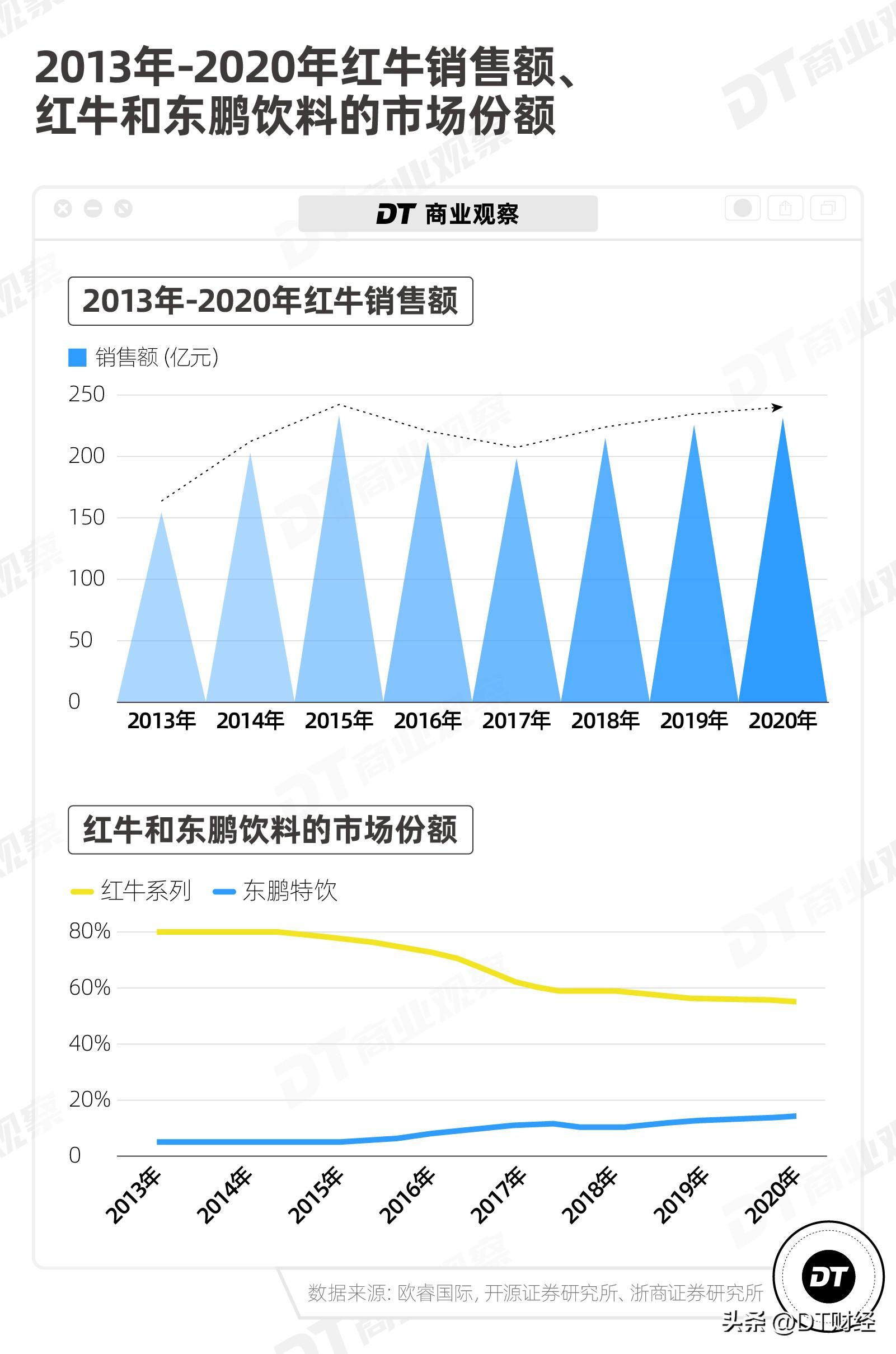

在当时,中国能量饮料市场还是红牛一家独大,占了超过8成的市场份额。

18年后,这家小厂成功上市。把它从濒临破产拉回来的产品,叫做“东鹏特饮”。

在上市前发布的招股书中,东鹏饮料引用欧睿国际的数据,说2019年 “东鹏特饮”已经成为中国能量饮料市场的老二,市场份额仅次于红牛(前三名分别是:红牛57%、东鹏15%、乐虎10%)。

在后续的财报中,东鹏饮料不再提市场份额,而是引用尼尔森 IQ 的数据,强调东鹏特饮从2021年起销量就超过红牛成为行业第一,并且销量占比还在不断提升。

东鹏特饮到底有没有超越红牛,确实存在不同口径的答案。但不管在哪个口径,都能证明,这家从破产边缘爬起来的企业,靠着一款饮料,快速增长,不断抢夺红牛的市场份额。

东鹏特饮是怎么做到的?

在进入东鹏饮料厂前,林木勤在一家中国红牛的代工厂工作,很熟悉红牛的产品和运作。

早在1998年,他就尝试在东鹏开发能量饮料“东鹏特饮”并上市售卖。

这款饮料从包装到成分、口味都跟红牛很相似:黄底蓝字的罐装包装、口味大同小异、而且都在产品中添加了牛磺酸、咖啡因、肌醇、维生素B等成分。

不过在当时,东鹏饮料厂的主推产品是广东地区纸盒饮料的“老三样”:菊花茶、清凉茶和冬瓜茶。林木随开发的东鹏特饮并没有被重视。

直到2003年,经营不善的东鹏饮料厂濒临破产。

2003年到2009年,接手东鹏的林木勤干了两件事:一边是继续卖“老三样”但严格把控价格和成本,先把厂子开下去:连续7年,菊花茶都卖一盒1元,利润2-3分,靠着薄利多销维持运转;另一边,他也没有放弃能量饮料,握着红牛的经验和技术,继续寻找突破口。

林木勤仔细研究过可能需要能量饮料的消费者:首先是货车司机、出租车司机和厂哥厂妹,他们不仅需要精神上的提神醒脑,更需要补充体力;此外,菜商小贩、水产老板这些为了讨生活经常昼夜颠倒、保持清醒的人也是它的目标用户。

他得出结论,在当时的中国市场,蓝领才是能量饮料的刚需人群。

也是这段时间,红牛已经逐渐成为中国能量饮料市场的霸主。2003年,红牛公司成为NBA在中国的合作伙伴,还赞助了翼装飞行、钱塘江国际冲浪赛、全国羽林争霸等比赛;2008年,红牛以1.6亿元价格拿下央视北京奥运广告资源第一标。

红牛还把刚进入中国时的广告语“汽车要加油,我要喝红牛”,换成了“渴了喝红牛,困了累了更要喝红牛”。

换句话说,已经打开市场的红牛,正在把目标用户从蓝领扩大为中高端人群:比如写字楼里的白领、极限运动爱好者……

红牛在向上,东鹏则决定从“下沉”突围,蓝领,仍然是蓝领。

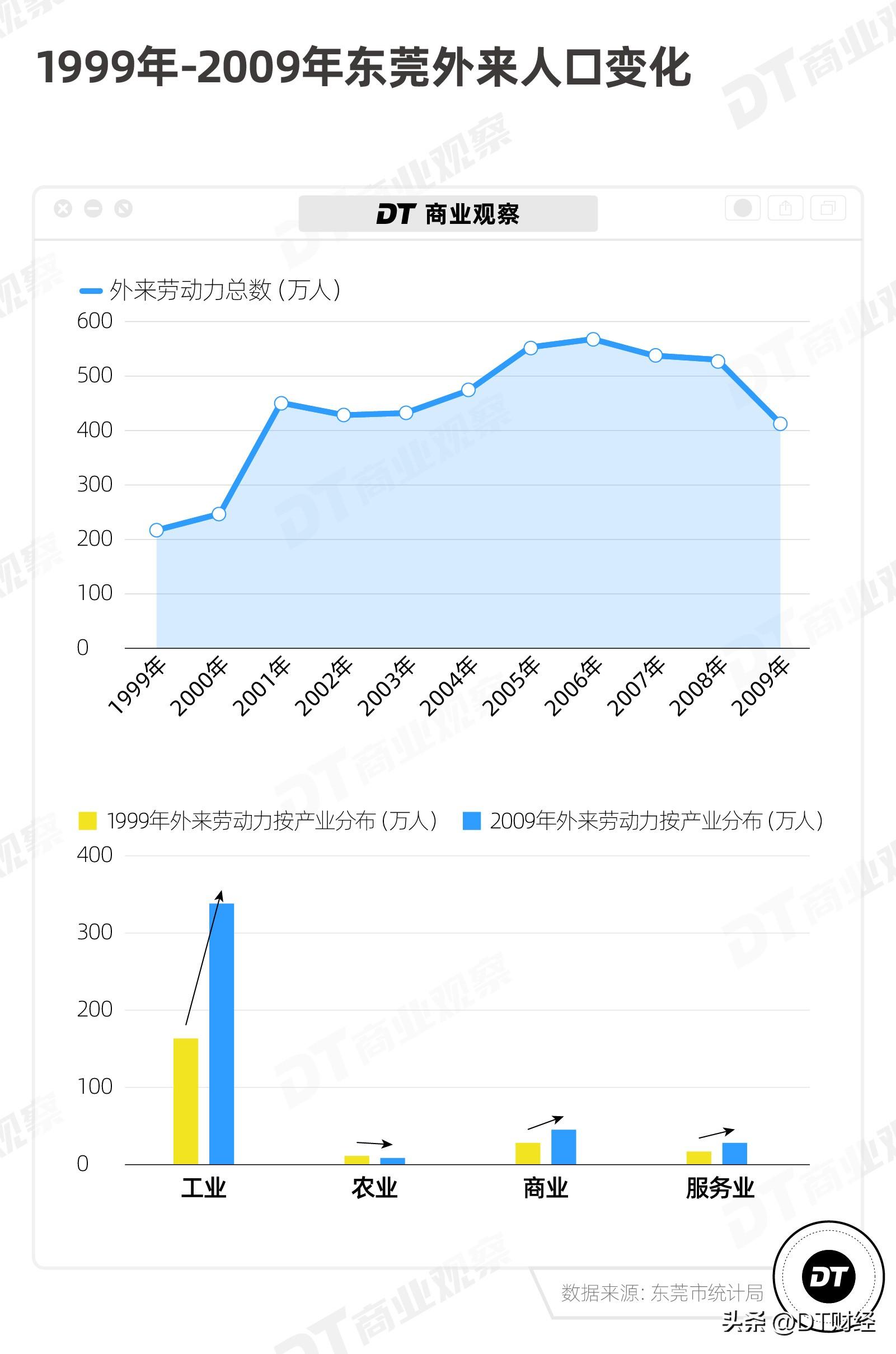

2009年,林木勤重启能量饮料,虽然东鹏的公司在深圳,但他选择把东莞作为第一个样板城市。

为什么是东莞?《DT商业观察》查看了东莞市统计局发布的统计年鉴,发现这段时间,正是东莞外来劳动力数量爆发的时期,而这些人,大多去做了蓝领:

1999年,东莞外来劳动力从事工业和服务业的人数分别是161万和15.5万,到了2009年,东莞这两大产业外来劳动力已经分别达到了336万和27万,翻了近两倍。

林木勤当时放话:“东莞作为东鹏特饮的样板市场,如果做不到1个亿,就不要走出去。”

当然,在“无资金,无品牌,无依靠”的情况下,直接复制红牛显然是没用的。

多年的探索让林木勤意识到,虽然市场已经接受了红牛,但在他看中的下沉市场,红牛还有一些明显的问题:

首先是价格太高。红牛官方定价6元一罐,一罐250ml,这个价格放到现在来看也不算便宜,更何况当时,饮料的主流价格带是1到3元。

其次,红牛的包装不方便。像货车司机、建筑工人这样的群体,大多是在有灰尘的环境里工作,红牛的易拉罐设计对他们不太友好,一旦拉开,就必须及时喝完——因为工厂里、工地上,灰尘太多,没法开口放着。

因此,新的东鹏特饮,针对这两点,去做差异化。

2009年,一款全新包装的东鹏特饮上市:同样是250毫升,红牛卖6块,东鹏只卖3块;红牛用易拉罐,东鹏用塑料瓶装,不仅比罐装节约成本,还额外加了个防尘外盖。

在核心成分差不多的情况下,东鹏的价格直接打到了红牛的一半。

此外,新的东鹏还加了一个防尘外盖:

内盖,需要逆时针旋转才能拧开,外盖,是个塑料做成的透明体,手掌握住它往上一提,就能打开。

(左一、左二为瓶装东鹏特饮,外瓶盖设计保留至今/东鹏特饮官网)

(左一、左二为瓶装东鹏特饮,外瓶盖设计保留至今/东鹏特饮官网)设计之初,外盖有两个作用,一是防尘,二是分享。

不过,林木勤应该也没想到,这个不起眼的外盖,在日后,成了千千万万个货车司机的专用烟灰缸,以及钓鱼爱好者们酷爱的鱼饵杯。

在知乎上,“东鹏特饮外面那层透明的盖子有什么用?”这个问题被浏览了四百多万次,远远高于“东鹏特饮,乐虎,红牛哪个好一些?”“东鹏特饮效果咋样”“东鹏特饮喝多了会怎么样”等问题的浏览量和讨论度。

这个神奇的外瓶盖,成了许多人尤其是长途司机选择东鹏而不是红牛或者其他品牌的决定性因素,除了防尘,它还能:

开车途中无处掸烟灰,外盖拿下来,就是烟灰缸;

开车时一只手喝水,抠掉里盖,直接用外盖,一只手就可以怼开;

在开车的颠簸场景中,如果是易拉罐开完之后必须喝完,不然容易洒;

当鱼饵量杯,而且因为会沾上饮料里的牛磺酸,吸引鱼;

当大米的量杯;喂狗子喝水;盖蟑螂……

……

(华与华营销咨询有限公司董事长华杉微博)

(华与华营销咨询有限公司董事长华杉微博)这种靠小细节获得消费者的芳心在饮品界比比皆是:

另一款运动饮料——尖叫,靠着这独特的瓶盖设计,从能量饮料变呲水枪和调料瓶,霸占小学生和小摊贩的市场,在能量饮料界一直占有一席之地。

可口可乐也曾通过把冰箱货架倾斜10度这个小细节,提高自己的销量:顾客拿了饮料马上后面饮料就把前面位置顶了,一方面是让顾客不好意思放回去,另一方面是马上把位置顶了,如果要还回去、再拿别家的饮料要花费更多时间。

别出心裁的设计加上误打误撞的运气,2009年,这款新包装的东鹏特饮一上市,当年就卖了2万箱,2012年,销售额破亿。

林木勤意识到,该让东鹏走向全国了。

为了提高东鹏特饮知名度,2013年,林木勤花了大价钱签约谢霆锋作为品牌代言人。同一年,红牛舍弃了广告语“渴了喝红牛,困了累了更要喝红牛”,东鹏直接换了个顺序,把自己家的广告语改成“累了困了喝东鹏特饮”,并沿用至今。

2015年,东鹏在保留“累了困了喝东鹏特饮”广告语的同时,推出“年轻就要醒着拼”的slogan,在它的广告片中,主角除了工人、外卖骑手,还有白领、学生,饮用场景多了加班、运动、娱乐等场景。

看上去,就像当年的红牛一样,在占领蓝领市场后,东鹏也想扩大自己的受众,向年轻群体进军。

不过,如果仅从市场份额来看,2013年到2015年的东鹏市占还只是在缓慢爬升。它的市占率迅速增长,是在2015年之后。

一个重要的原因是,这一年,最大的对手红牛陷入商标争议,由于商标所有权不明确,华彬集团不能对红牛进行广告宣传,从2015年到2017年,红牛销量额连续两年下滑,市场份额也随之下降。

趁着老大红牛内乱,东鹏、乐虎等其他能量饮料品牌迅速崛起,抢夺市场,无一例外,他们都盯上了年轻人。

便宜和包装是东鹏征服广东蓝领的杀手锏。到了更广泛的年轻人群体,该怎么办?

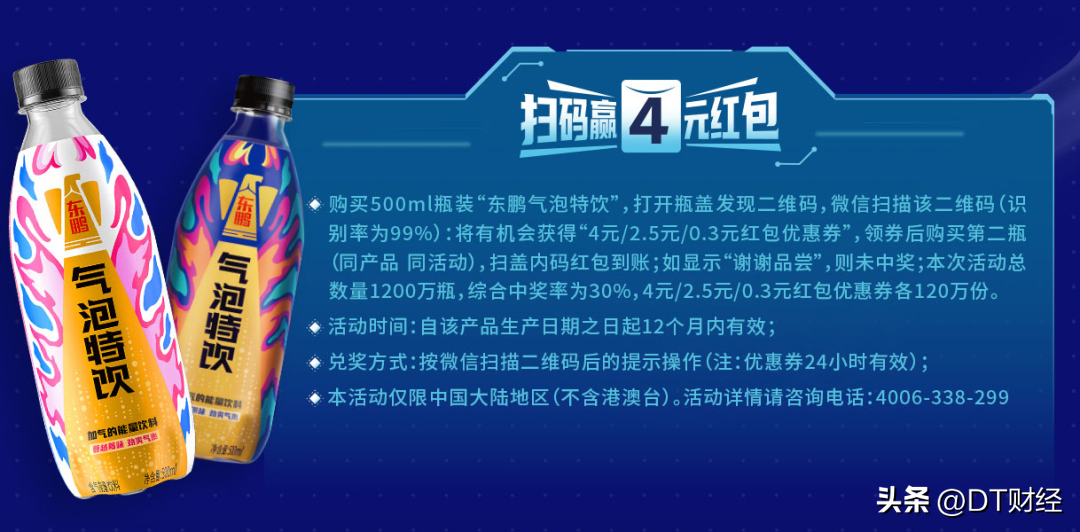

为了能在一众对手中跑出来,东鹏特饮使出了一招:给所有消费者送钱。

2015年春晚,微信与春晚合作推出摇一摇红包,带火了微信红包。

林木勤看到微信红包时灵光一闪:既然红包可以塞到一个电子信封里去发,那可不可以把一个二维码放到瓶盖里面,让消费者扫码,将红包直接发送到消费者手上。

比起“再来一瓶”,这种返利方法不仅更新鲜,还避免了消费者去店里兑换的麻烦、解决了假瓶盖冒领的难题。

根据东鹏特饮的过往推送,从2015年起,东鹏推出了各种扫瓶盖领红包的活动:

中奖几率从30%到 100%不等,金额有8.8元、88元、888元、520元的……反正一瓶只要3块,几率比买彩票高得多,扫到就是赚到,没扫到也不亏。

(图片来源:东鹏特饮官公众号)

(图片来源:东鹏特饮官公众号)在其他地方,东鹏也没少刷脸。

《DT商业观察》查看了2018年到2023年上半年的费用,总体的销售费用和宣传推广费率在降低,但2018年格外高;2019年、2021年也有小高点。

展开来看2018年到2021年东鹏特饮宣传推广费构成:2018年,电视电台广告最高,主要是因为世界杯;另外,2019年的户外广告和2021年新增的渠道推广费,也是两个明显的上升点。

2019年的户外广告,是在加油站、服务区、地铁、公交车、候车亭这些地方频繁露脸:光是2019年,东鹏就投放了1800多辆公交车、1700多块候车厅、2800多块墙体、400多块T牌……只要你一出门,就让你感觉全世界都在“累了困了,就喝东鹏特饮”。

2021年的渠道推广费,则是投放冰柜:东鹏专门拿出一笔钱给夫妻杂货店、小卖铺、传统商超的老板们,如果他们在冰柜中能够摆放一定排数的东鹏特饮,在一个月之后就能直接拿到激励。

如果说,扫码返红包是给消费者送钱,投放冰柜则是给店家送钱,东鹏为了让自家产品露脸、提高知名度,着实花了一番功夫。这些动作也确实给东鹏带来了市场份额的持续提升。

不过,问题来了:抛开返利带来的刺激消费,除了蓝领们,还有谁是东鹏特饮的刚需用户?针对他们,东鹏做了什么?

早些年林木勤就留意到,除了加油站便利店、高速公路服务区、传统小卖店这些地方,还有两个线下场所是卖能量饮料的好地方:一个是网吧,一个是KTV。

也就是说,除了干体力活的人群需要补充能量,娱乐的年轻人也需要能量。放到现在,喝能量饮料更具体的场景可能是:熬夜打游戏、熬夜看球的、健身的、蹦livehouse……

从品牌的广告动作来看,东鹏特饮格外关注体育赛事和电竞赛事。

2015年女排世界杯上,东鹏特饮就以广告贴片的形式试了水。

(图片来源:东鹏特饮公众号)

(图片来源:东鹏特饮公众号)2017年之后东鹏特饮密集在体育和电竞赛事上发力:

2017年,赞助了NESO全国电子竞技公开赛;

2018年成为FFIFA世界杯转播赞助商;

2019年赞助中超联赛、成为CEC中国汽车耐力锦标赛的官方唯一指定能量饮料;

2022年卡塔尔世界杯,同一年成为KPL王者荣耀职业联赛官方指定功能饮料;还赞助了中国街舞联赛……

也就是说,新的核心用户可能是都市里的球迷和电竞爱好者。

另一组数据或许可以辅助这个结论。

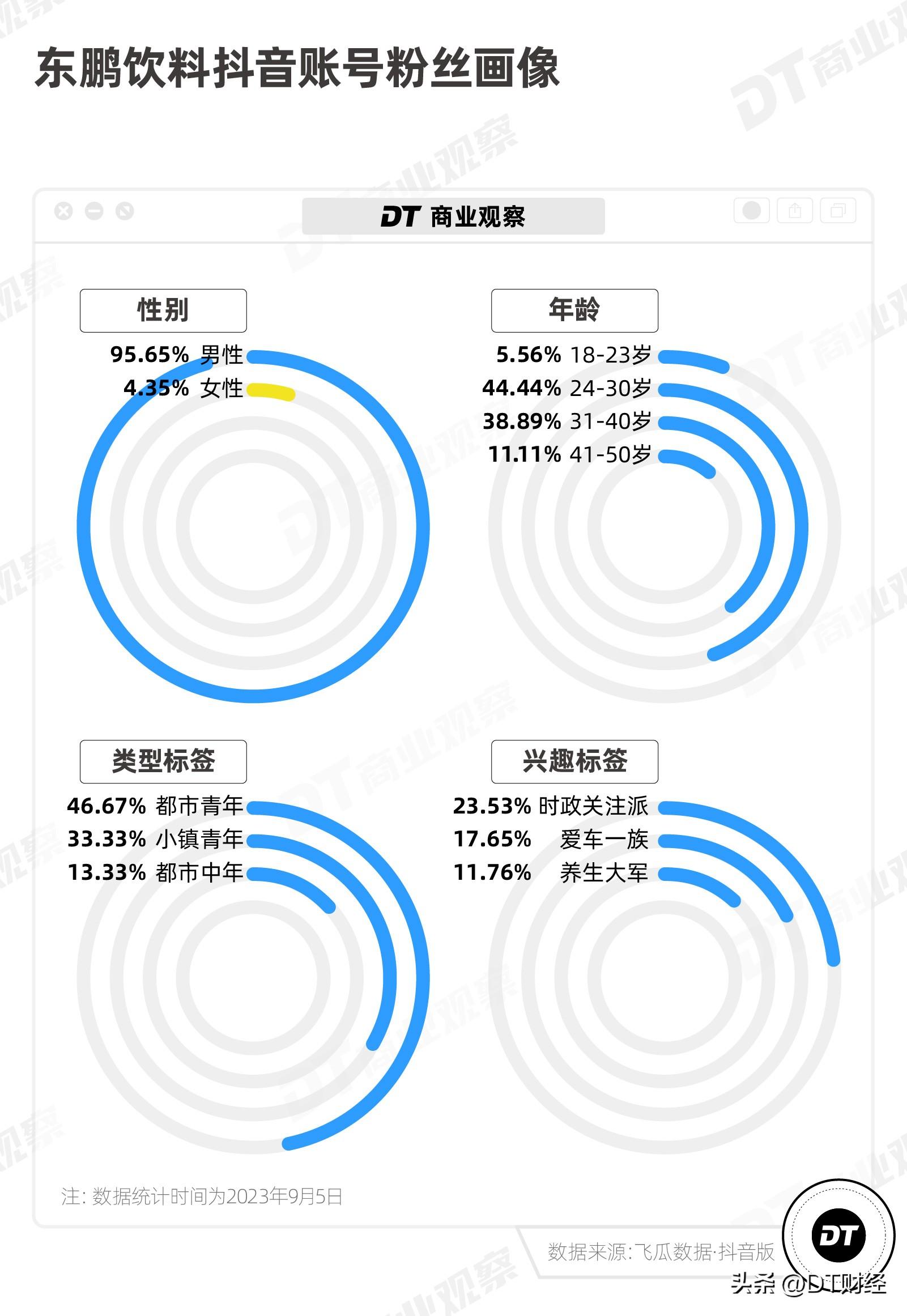

《DT商业观察》浏览了社交媒体上关于东鹏特饮的讨论,发现在小红书上东鹏特饮几乎没有任何声量;抖音上相对多一些。我们进一步查看了东鹏特饮抖音店铺的粉丝画像,结果发现,它的受众主要是24-40岁的男性,超过4成是都市青年,比较关注车和时政。

2022年,因为增长放缓,一度有媒体唱衰东鹏,原因是产品单一,“大单品”东鹏特饮就贡献了9成收入,但它的受众货车司机在衰老,数量在下降。

2023年上半年,东鹏新的业绩打脸了这一说法,销售收入从去年同期的41.18亿元上涨至51.35亿元,增速又回来了,而高增长,依旧是靠东鹏特饮。

毕竟,它的受众早已不仅仅是司机,还有外卖骑手、快递小哥,以及,熬夜看球的球迷、打游戏的电竞爱好者、加班的白领。

在庞大的中国,仍然有一大群人需要这种平价提神的饮料,可能是因为工作,也可能是为了娱乐,反正仍然有庞大的群体,经常“累了、困了”。

而面对“只有一个大单品”的问题,东鹏有在努力发展第二增长曲线,除了能量饮料,近两年还推出了即饮咖啡(东鹏大咖)、电解质饮料(东鹏补水啦)、饮用天然水(东鹏水)等新品,走的也是能量饮料成功的老路子:

所有产品都走性价比路线;新品先在广东试点,卖得好再走向全国;推广方式延续瓶盖扫码返红包……

(在新品上仍然采取了扫瓶盖二维码返红包的推广形式 /东鹏特饮官网)

(在新品上仍然采取了扫瓶盖二维码返红包的推广形式 /东鹏特饮官网)不过,在饮用水、咖啡、电解质饮料这些赛道上,格局与当年能量饮料已经大不相同:饮用水早已巨头林立,牢牢把控渠道;即饮咖啡在下沉市场没有强烈的需求;电解质饮料有宝矿力、外星人、尖叫这些对手……

没踩上时代的东风、没有别出心裁的产品亮点或营销打法,东鹏特饮的神话,恐怕在其他单品上很难复制。

(头图来源:@东鹏特饮官方微博)

数据家股东披云网络科技集团有限公司减持80.74万股 股东段振增持80.74万股

挖贝网5月8日,数据家(837528)发公告称,2023年5月8日,披云网络科技集团有限公司通过大宗交易减持挂牌公司807,400股,拥有权益比例从40.00%变为35.00%。2023年5月8日,段振通过大宗交易增持挂牌公司807,400股,段振及其一致行动人拥有权益比例从60.00%变以为65.00%。0001巴铁让中国吃了一个大亏?给43年租期却修了14年,中国真的亏了吗

巴铁,这是中国人对巴基斯坦人民的亲切称呼。两国之间有着深厚的友谊和密切的合作,尤其是在基建、经济、贸易、科技等方面。不过,有一个话题引起了很多人的关注和争议,那就是巴基斯坦把瓜达尔港租给中国43年,而其中14年是中国用来修建的时间。也就是说,中国实际享受的租期还不足30年。这样看来,中国是不是吃了一个大亏?我们为什么要租用这个港口?这个港口有什么价值?大财经2023-11-09 20:12:170001联想官网驱动下载 联想电脑驱动下载官网

【搞科技教程】也知道不少的人在找联想A860E的usb驱动,今天在这里就来给大家分享一下了,这个驱动也是联想手机专用的驱动,为什么要分享驱动呢,因为在论坛里很多人对手机进行操作的时候老是提示电脑识别不了手机,要不就是连接不上,总是出现这样或那样的问题,出现这些问题的主要原因就是电脑上没有安装驱动造成的,下面就来给大家分享一下这个手机的专用驱动的吧,有需要的可以下载下来备用了。大财经2023-03-23 05:33:210001